All Categories

Featured

Table of Contents

Indexed universal life plans provide a minimal surefire interest price, additionally recognized as an interest crediting flooring, which minimizes market losses. Claim your cash money worth sheds 8%.

It's likewise best for those ready to think extra risk for greater returns. A IUL is a permanent life insurance policy plan that obtains from the residential properties of a global life insurance policy policy. Like global life, it allows flexibility in your survivor benefit and costs payments. Unlike global life, your money value expands based on the efficiency of market indexes such as the S&P 500 or Nasdaq.

What makes IUL different from other plans is that a section of the premium settlement goes into yearly renewable-term life insurance policy (IUL plans). Term life insurance policy, likewise referred to as pure life insurance policy, guarantees survivor benefit settlement. The remainder of the worth enters into the general cash money worth of the plan. Bear in mind that fees should be deducted from the worth, which would decrease the cash worth of the IUL coverage.

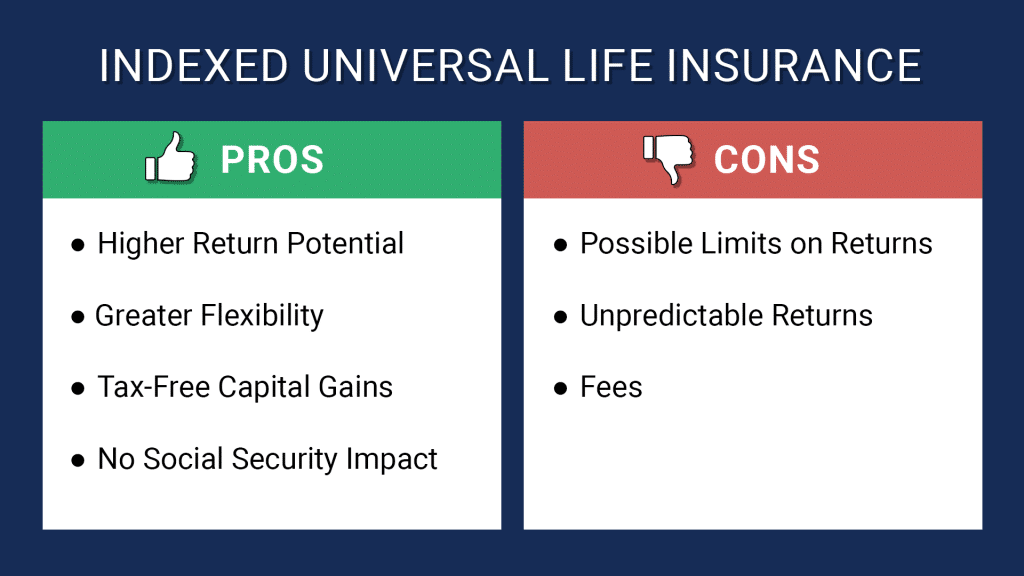

An IUL plan may be the ideal selection for a client if they are seeking a long-lasting insurance coverage product that develops wealth over the life insurance policy term. This is because it supplies potential for growth and additionally retains one of the most worth in an unstable market. For those who have significant possessions or wealth in up front financial investments, IUL insurance will be a fantastic wealth monitoring device, especially if somebody wants a tax-free retired life.

How much does Guaranteed Iul cost?

In comparison to various other plans like variable global life insurance policy, it is much less risky. When it comes to taking treatment of beneficiaries and taking care of wealth, here are some of the leading reasons that somebody might pick to choose an IUL insurance plan: The cash worth that can build up due to the rate of interest paid does not count towards earnings.

This implies a client can utilize their insurance policy payout rather than dipping into their social security money prior to they prepare to do so. Each plan needs to be customized to the customer's individual requirements, particularly if they are taking care of sizable possessions. The policyholder and the agent can choose the amount of danger they take into consideration to be suitable for their requirements.

IUL is an overall easily adjustable plan. As a result of the interest prices of global life insurance policy policies, the price of return that a customer can possibly obtain is greater than various other insurance coverage. This is due to the fact that the proprietor and the representative can utilize call options to raise possible returns.

How do I cancel Indexed Universal Life Insurance?

Policyholders may be brought in to an IUL policy because they do not pay resources gains on the added cash worth of the insurance plan. This can be contrasted to other policies that call for tax obligations be paid on any kind of money that is gotten. This means there's a cash money property that can be obtained at any kind of time, and the life insurance coverage policyholder would certainly not need to bother with paying taxes on the withdrawal.

While there are several advantages for a policyholder to select this kind of life insurance policy, it's not for everyone. It is vital to let the consumer recognize both sides of the coin. Here are some of the most important things to motivate a customer to think about prior to deciding for this choice: There are caps on the returns a policyholder can get.

The ideal choice depends upon the client's risk tolerance - Indexed Universal Life financial security. While the costs connected with an IUL insurance coverage policy are worth it for some consumers, it is necessary to be ahead of time with them concerning the prices. There are superior cost charges and other administrative charges that can start to build up

No ensured interest rateSome various other insurance plan provide a rates of interest that is ensured. This is not the situation for IUL insurance policy. This is fine for some, yet for others, the unidentified fluctuations can leave them feeling subjected and insecure. To read more regarding managing indexed universal life insurance policy and recommending it for certain clients, get to out to Lewis & Ellis today.

How do I cancel Indexed Universal Life Protection Plan?

Consult your tax obligation, lawful, or accounting expert regarding your private situation. 3 An Indexed Universal Life (IUL) policy is ruled out a protection. Costs and survivor benefit kinds are flexible. It's attributing price is based on the performance of a supply index with a cap rate (i.e. 10%), a flooring (i.e.

8 Irreversible life insurance policy contains two kinds: whole life and global life. Cash worth grows in a getting involved whole life policy with returns, which are declared each year by the company's board of supervisors and are not assured. Money value expands in a global life policy via attributed interest and reduced insurance policy prices.

Can I get Indexed Universal Life For Retirement Income online?

Regardless of exactly how well you prepare for the future, there are occasions in life, both expected and unanticipated, that can impact the monetary health of you and your loved ones. That's a reason for life insurance policy. Survivor benefit is typically income-tax-free to beneficiaries. The survivor benefit that's normally income-tax-free to your recipients can help guarantee your family members will have the ability to maintain their criterion of living, help them maintain their home, or supplement shed income.

Points like possible tax obligation increases, rising cost of living, monetary emergency situations, and preparing for occasions like college, retired life, and even wedding celebrations. Some kinds of life insurance policy can aid with these and other issues as well, such as indexed global life insurance policy, or merely IUL. With IUL, your policy can be a funds, due to the fact that it has the potential to build value in time.

You can pick to obtain indexed rate of interest. Although an index might impact your passion attributed, you can not invest or directly participate in an index. Below, your plan tracks, yet is not in fact invested in, an external market index like the S&P 500 Index. This theoretical instance is attended to illustrative objectives just.

Fees and costs might decrease plan values. You can additionally select to get fixed interest, one collection foreseeable interest rate month after month, no issue the market.

Who has the best customer service for Indexed Universal Life Policyholders?

That leaves extra in your plan to potentially keep expanding over time. Down the roadway, you can access any type of readily available cash value through policy car loans or withdrawals.

{kind=link}

Latest Posts

New York Life Variable Universal Life Accumulator

The Cash Value In An Indexed Life Insurance Policy

Guaranteed Universal Life Insurance Quotes